Topics

How to Enter Housing Loan Information?

How is Tax Exemption from Interest on Housing Loan Calculated?

Proof Submission for Housing Loan Declaration

How to Enter Housing Loan Information?

If you have a housing loan and wish to enter information on your income from house property, you can enter information here. You will be eligible to claim tax rebate on the interest component of your repayment during the year Apr-March by entering information under the "Home Loan" tab.

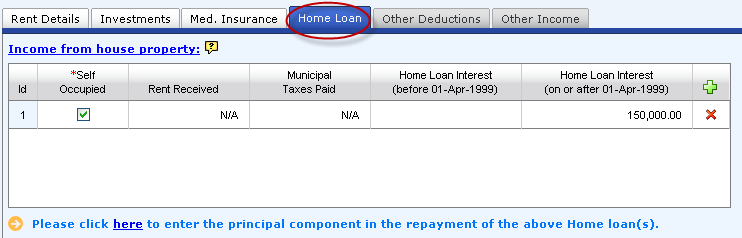

As soon as you click on the ![]() icon on top of the right extreme column in the table, you will see a row with blank fields appearing inside the table, where you can enter details of home loan interest that you have paid or will be paying for the year. Please click on the respective cells to update the required details.

icon on top of the right extreme column in the table, you will see a row with blank fields appearing inside the table, where you can enter details of home loan interest that you have paid or will be paying for the year. Please click on the respective cells to update the required details.

Fields

Self Occupied: Please select the checkbox if the property is self occupied. Once you select the "Self Occupied" field in any row, the "Rent Received" and "Municipal Taxes Paid" fields will automatically get disabled.

Rent Received: Please enter the rent amount received (in Rs) for the accommodation. The amount can have a maximum of two decimal places.

For any property which is not self occupied, you have to enter a value (other than zero) in the "Rent Received" field

Municipal Taxes Paid: Please enter the municipal taxes rent amount paid (in Rs) for the property. The amount can have a maximum of two decimal places.

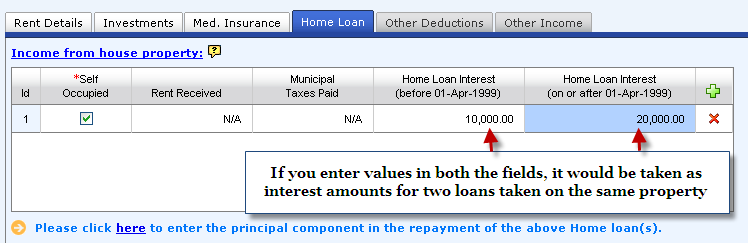

Home Loan Interest (before April 1, 1999): Please enter the total annual interest here if your home loan was taken before April 1, 1999. The amount can have a maximum of two decimal places.

Home Loan Interest (on or after April 1, 1999): Please enter the total annual interest here if your home loan was taken on or after April 1, 1999. The amount can have a maximum of two decimal places.

Interest on Housing loan – Self Occupied Property (Under Section 80EE): Exemption for Interest on housing loan for employees having an existing housing loan and self occupied by them, continues to restricted to a maximum of Rs. 2,00,000 (2 Lakhs). But for those employees who avail loan for the first time an additional exemption of up to Rs. 1,00,000 has been provided for the financial year 2013-2014. The maximum exemption shall be Rs 2,50,000 for such cases.

But the following conditions have to be satisfied to avail this additional exemption.

If this additional interest exemption in the year 2013-2014 is less than Rs. 1,00,000, the balance amount of interest up to Rs 1, 00,000 can be carried forward to the next financial year.

You can create as many rows as you wish to enter details in the respective fields. If you wish to delete any of the rows, you could do so by clicking on the ![]() icon at the end of the row.

icon at the end of the row.

Please note that you can enter interest on your housing loan here. In order to enter the principal amount repaid on your housing loan, please visit the "Investment - 80C" tab under the "Investments" tab. Click here to know more.

NOTE:

How is Tax Exemption from Interest on Housing Loan Calculated?

The Indian income tax law specifies tax deductions related to income from house property under Section 24 (b), wherein tax benefits can be availed on home loans on both the principal and interest components of a home loan. Irrespective of whether you have occupied or rented the house for which you have the loan, you can avail tax exemption. In addition, if you own a house on which you have a housing loan but you choose to live in a rented accommodation, you can claim both HRA exemption and housing loan tax exemption.

If you have occupied the property and your loan was taken before April 1, 1999

A maximum of Rs 30,000 can be availed as interest exemption and reduced from your salary in order to calculate the taxable income. In case your interest payment is lesser than Rs 30,000 for the current year, the interest exemption will be restricted to the actual interest amount paid.

The principal amount for the loan should be claimed under Section 80C -- which allows a maximum exemption of Rs. 1,50,000 (1.5 Lakhs) -- along with investments such as life insurance.

If you have occupied the property and your loan was taken on or after April 1, 1999

A maximum of Rs. 2,00,000 (2 Lakhs) can be availed as interest exemption and reduced from your salary in order to calculate the taxable income. In case your interest payment is lesser than Rs. 2,00,000 (2 Lakhs) for the current year, the interest exemption will be restricted to the actual interest amount paid.

The principal amount for the loan should be claimed under Section 80C -- which allows a maximum exemption of Rs. 1,50,000 (1.5 Lakhs) -- along with investments such as life insurance.

If your property is rented out

If the property is rented out, then the annual value (income as rent) will be calculated for that property as per the following formula.

Income from house property = Rental Income (net of municipal taxes) - 30% of rental income - Interest payable on home loans.

The income from house property can be negative when the interest payable is more that rent received. If the income from house property is a positive number, it is added to your salary for arriving at taxable income. If the income from house property is a negative number, it is reduced from your salary for arriving at taxable income.

Note:

1. Rental income should be reduced by municipal taxes, if any, paid for the property.

2. 30% of the rental income which is applied as a standard deduction is calculated automatically by Tanqaa once you enter the rental income.

3. In case of rented out properties, there is no limit on the interest amount that will be considered for tax exemption.

The principal amount for the loan should be claimed under Section 80C -- which allows a maximum exemption of Rs. 1,50,000 (1.5 Lakhs) -- along with investments such as life insurance.

If you have multiple "self-occupied" properties

In case, you have two properties where you have occupied one and kept the other property vacant, then the vacant property is "deemed to have been let-out" as per the Indian tax law. On Tanqaa, you can only mark one property as a self-occupied property. When you enter details of the vacant property by creating a new row, please enter a notional rental income in the "Rent Received" field. The notional rental income is the amount you would have received as rental income had you let it out and should be arrived at in line with the guidelines of the Indian tax department. Please note that in case of "deemed to be let out" properties, there is no limit on interest on housing loan considered for the purpose of tax exemption calculation.

Some rules to remember:

Proof Submission for Housing Loan Declaration

The details of the required proof and guidelines are given below for your reference.

Housing Loan |

Proof to be submitted |

Guidelines |

Income / Loss on Home Loan Property under Section 24 (b) |

|

|

Copyright , Tandem Integrated Business Solutions Private Limited